The APR is used when quoting figures for loans so that extra charges and commissions cannot be hidden. APR (annual percentage rate) takes the base percentage rate for a loan or credit agreement and then incorporates charges and fees that the base rate does not cover.

For instance charges for the credit, amounts payable to complete the loan, administration charges, annual fees, and anything else payable for the duration and/or completion of the loan or credit agreement. Get tips on how to manage credit cards effectively.

This works fine for a fixed loan where everything remains stable over a period of time, under these circumstances the APR reflects the actual interest paid over and above the amount of the original loan, and so is the true cost of the loan.

Credit cards however are charged on a monthly basis with no fixed repayment amount apart from the minimum stipulated by the terms of the credit card.

The problem with working out an annual amount of interest for a credit card is that the amount of interest paid is dependent on the amount of outstanding balance left over each month.

Interest is compoundable, which means the interest in one month itself attracts interest the following month since it becomes part of the outstanding balance. The credit score rating is automatically calculated on the account access web portal.

To help standardize APR’s and help consumers compare the true cost of credit cards the Department of Trade and Industry released criteria in the Consumer Credit (Advertisements) Regulations 2004 that must be assumed by credit card companies when calculating APR’s.

The assumptions for UK credit cards are that an initial amount of $1500 is taken out on that credit card, that repayments are made starting one month later and repaid in 12 equal installments.

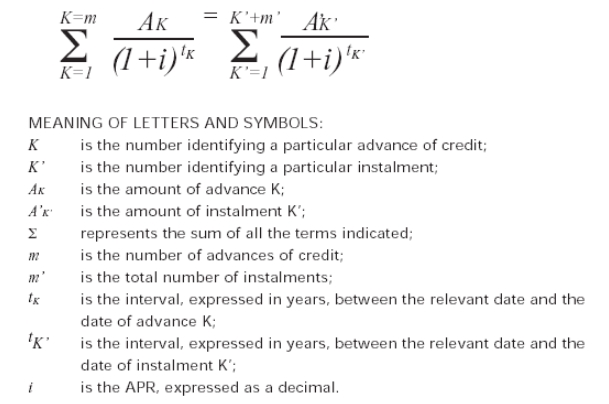

The actual formula for working out APR is a complicated one.

A simplified formula for working out APR is (1+m)^12-1, where m is the monthly rate.

So APR for US credit cards is based on a notional example of a starting balance of $1500 and this is paid off in equal monthly installments resulting in a nil balance 12 months later.

This is a fair way of comparing rates between different credit cards but is not really of much use to work out what you are likely to pay in interest in a real-life situation.

In reality, it will be far more practical to look at the monthly rates being offered by credit card companies if you wish to work out the amount of interest you will pay in a given period.

Just remember that interest is compounded so any interest attracted in a given month will itself attract interest in the next month if not paid in full. Another point to remember is that purchases, balance transfers, and cash advances may all attract different rates of interest.

Be careful not to fall into the trap of believing the APR is 12 x the monthly rate. It is not!

Remember APR is an annual rate that takes the base interest rate, includes any hidden charges, and assumes a balance is carried forward each month.